Bitcoin

Bitcoin  Ethereum

Ethereum  Tether

Tether  XRP

XRP  BNB

BNB  USDC

USDC  Solana

Solana  TRON

TRON  Figure Heloc

Figure Heloc

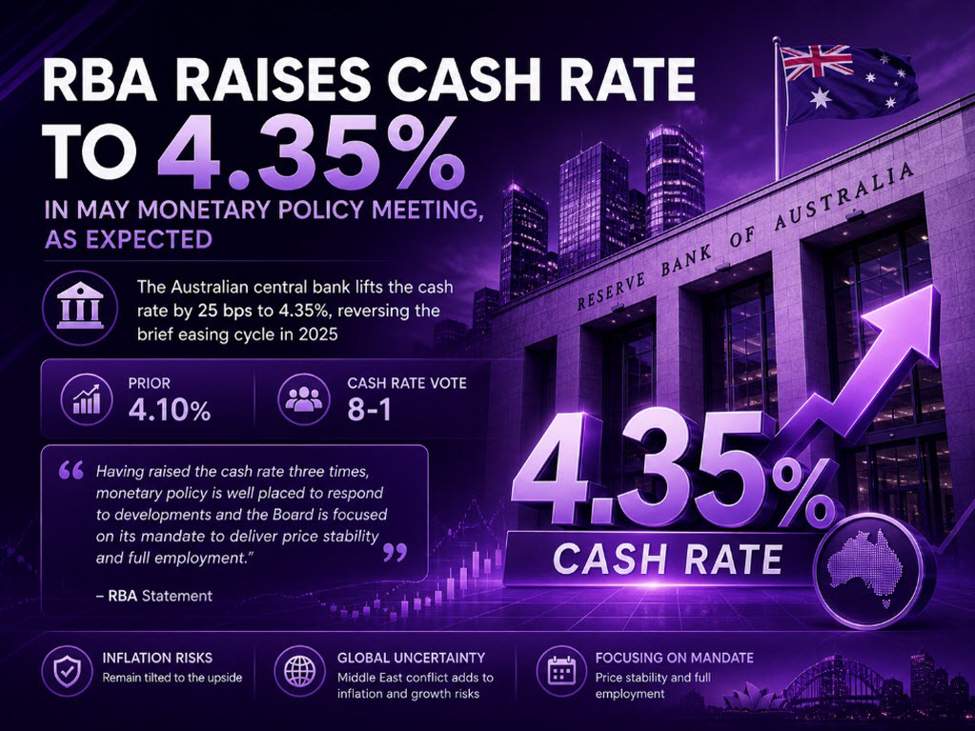

Prior 4.10%Cash rate vote was 8-1Middle East conflict has resulted in sharply higher fuel and commodity prices, which are already adding to inflationThere are early signs that many firms are looking to increase prices of their goods and servicesThere are materially heightened uncertainties about the outlook for domestic economic activity and inflationThere are plausible scenarios where inflation is higher and activity lower than envisaged under the baseline forecastThere are indications that Middle East conflict could lead to second-round effects on prices for goods and services more broadlyInflation is likely to remain above target for some time and that the risks remain tilted to the upsideHaving raised the cash rate three times, monetary policy is well placed to respond to developmentsFocused on mandate to deliver price stability and full employmentWill do what it considers necessary to achieve that outcomeFull statementThe key passage in all of this is this one right here: “Having raised the cash rate three times, monetary policy is well placed to respond to developments and the Board is focused on its mandate to deliver price stability and full employment.”That’s as clear a signal as any that they are leaning towards being on the sidelines until they get better clarity on how Middle East developments will impact the inflation outlook further.Adding to that, they subtly toned down their language slightly after having said in March that risks to inflation have “tilted further to the upside”. This time around, they’re saying that risks to inflation “remain tilted to the upside” only. It’s not much but it is some indication of also erring more towards staying pat in June.Besides that, the RBA notes that their baseline forecast is for “the conflict is resolved soon and fuel prices decline” but also “sees underlying inflation peaking higher than was expected in February”. However, they at least acknowledge that there could be scenarios in which the outcome is worse than what they are forecasting.But either way for now, they might be more comfortable moving to the sidelines after three straight rate hikes to undo the entire easing cycle from 2025.Coming into the meeting, traders were pricing in ~85% odds of a 25 bps rate hike with ~61 bps of rate hikes priced by year-end.AUD/USD is just marginally up on the decision but not really doing much, keeping flattish now at 0.7165 on the day.

This article was written by Justin Low at investinglive.com.

💡 DMK Insight

Rising commodity prices from the Middle East conflict are shaking up inflation expectations, and here’s why that matters: With the cash rate vote recently at 4.10% and an 8-1 split, traders should be on high alert. Higher fuel and commodity prices are not just a short-term blip; they signal a potential shift in consumer behavior as firms start to pass costs onto consumers. If inflation continues to rise, we could see central banks tightening monetary policy more aggressively, which would impact everything from forex pairs to crypto assets. Keep an eye on inflation metrics and central bank communications, as they could dictate market sentiment in the coming weeks. But here’s the flip side: if firms are cautious about raising prices due to economic uncertainties, we might see a slowdown in consumer spending, which could ease inflationary pressures. This creates a tug-of-war scenario for traders. Watch for key economic indicators and sentiment shifts that could signal whether inflation is truly entrenched or if we’re headed for a cooling period. Pay attention to the next inflation report and any central bank meetings for potential market-moving insights.

📮 Takeaway

Monitor inflation reports closely; a sustained rise could trigger aggressive central bank actions, impacting forex and commodity markets significantly.