Bitcoin

Bitcoin  Ethereum

Ethereum  Tether

Tether  XRP

XRP  BNB

BNB  USDC

USDC  Solana

Solana  Figure Heloc

Figure Heloc

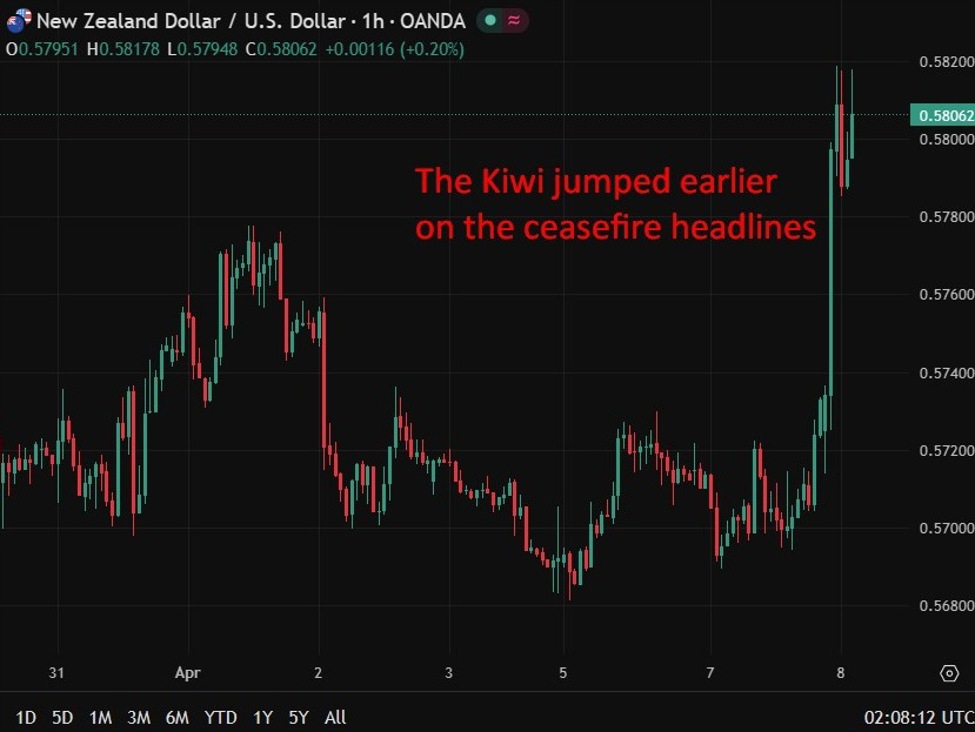

more to come- Full statement etc. here. Summery:RBNZ holds OCR at 2.25% amid Middle East-driven shock

Inflation set to rise sharply, peaking around 4.2% near term

Growth outlook weakens as energy costs hit demand

Policy focused on medium-term inflation and expectations

Financial conditions already tightening domestically

Risks skewed to stagflation: higher inflation, weaker growth

RBNZ signals readiness to hike if inflation persistsIn brief:Policy decision and contextThe Reserve Bank of New Zealand Monetary Policy Committee agreed to hold the Official Cash Rate at 2.25%, as escalating geopolitical developments have materially shifted the economic outlook. Since the February Monetary Policy Statement, the conflict in the Middle East has significantly altered the balance of risks, with policymakers now facing a more complex trade-off: near-term inflation is expected to rise sharply, while economic activity is set to weaken. The Committee emphasised it remains vigilant to broader inflation pressures and stands ready to act if needed to ensure inflation returns to target over the medium term.Global backdrop: supply shock and financial volatilityThe conflict has triggered a major global supply shock, disrupting energy flows through the Strait of Hormuz and pushing up oil and refined product prices. These developments are feeding through into global supply chains, lifting inflation while weighing on growth across many economies.Financial markets have reacted with heightened volatility. Equity markets have declined in several regions, bond yields have risen, and the US dollar has strengthened, reflecting expectations of weaker global growth and tighter financial conditions.Despite these pressures, most major central banks have so far opted to keep policy rates unchanged, mirroring the uncertainty surrounding the duration and impact of the shock.Global inflation and growth outlookGlobal inflation, which had been trending lower, is now expected to reaccelerate in the near term due to higher energy costs, while growth momentum weakens. The impact is particularly acute for energy-importing economies, including many of New Zealand’s key trading partners in Asia.However, outcomes are expected to vary across countries depending on starting conditions, fiscal responses, and economic resilience, suggesting divergent monetary policy paths ahead.Domestic inflation outlookIn New Zealand, inflation is already above target and set to rise further. Annual CPI stood at 3.1% in Q4 2025, and the RBNZ now expects inflation to increase to around 3.0% in Q1 2026 and 4.2% in Q2, driven largely by higher fuel costs and spillovers into transport, food and other energy-sensitive components. The outlook remains highly uncertain, hinging on the evolution of the conflict and the persistence of supply disruptions. While futures markets imply some easing in oil prices later this year, the Committee sees risks skewed to higher prices.Domestic economic activityEconomic growth was already fragile prior to the shock, with GDP rising just 0.2% in Q4 2025. Although early indicators suggested a modest recovery, the conflict is now expected to dampen activity in the near term.Higher fuel costs are eroding household purchasing power and compressing business margins, while uncertainty is weighing on investment decisions. Recent data and business feedback indicate slowing activity and declining confidence, with some firms already passing on higher costs through surcharges, while others struggle to do so.Inflation dynamics and policy focusThe Committee reiterated that its focus remains firmly on medium-term inflation. The key issue is whether higher energy costs feed into broader wage- and price-setting behaviour, potentially leading to persistent inflation.Short-term inflation expectations are rising, but the RBNZ expects second-round effects to be limited by weak demand and spare capacity in the economy. This contrasts with 2022, when strong demand amplified inflation pressures following earlier global shocks.Maintaining anchored inflation expectations near 2% is critical. If core inflation or wage growth accelerates materially, the Bank signalled it would respond decisively.Financial conditionsDomestic financial conditions have already tightened since February. Wholesale interest rates have risen, mortgage rates have increased modestly, and the New Zealand dollar has weakened, adding to imported inflation pressures while providing some support to exporters.Liquidity conditions in local markets have also contributed to upward pressure on yields, reinforcing the tightening impulse.Risk assessmentThe Committee highlighted significant uncertainty and a wide range of possible outcomes.On the inflation side, risks include more persistent supply disruptions and a broader shift in pricing behaviour, which could lift core inflation and inflation expectations.On the growth side, risks include a sharper downturn in household spending, rising unemployment, and constrained business activity, particularly if access to key inputs such as fuel or fertiliser is disrupted.The balance of risks is asymmetric, with the potential for both higher inflation and weaker growth—effectively a stagflationary mix.Policy outlook and forward guidanceThe Committee debated the timing and magnitude of any future policy response. A pre-emptive tightening could help anchor expectations and limit second-round effects, potentially reducing the need for more aggressive hikes later.However, acting too early risks exacerbating the downturn in activity and employment, particularly if the inflation shock proves temporary.Ultimately, the Committee judged that holding the OCR steady best balances these competing risks at this stage. It will continue to monitor incoming data closely and stands ready to act decisively if inflation expectations begin to drift.

This article was written by Eamonn Sheridan at investinglive.com.

💡 DMK Insight

RBNZ’s decision to hold the OCR at 2.25% signals a cautious approach amid rising inflation pressures, particularly from Middle East tensions. With inflation expected to peak around 4.2%, traders should brace for potential volatility in the NZD as the central bank navigates a weakening growth outlook. Energy costs are likely to dampen demand, which could lead to stagflation risks. This scenario could pressure the RBNZ to adjust its policy sooner than anticipated, especially if inflation expectations continue to rise. Watch for key support levels in the NZD/USD pair; a break below recent lows could trigger further selling. Conversely, if inflation data surprises to the upside, expect a hawkish shift that could bolster the NZD. Keep an eye on upcoming economic indicators, particularly energy prices and inflation reports, as they’ll be crucial in shaping RBNZ’s future decisions and market sentiment.

📮 Takeaway

Monitor NZD/USD closely; a break below recent support could signal further downside amid rising inflation and stagflation risks.

![Stock markets soar as predicted [Video]](https://dmknewsbot.io/wp-content/uploads/2026/04/Equity-Index_SP500-1_Medium.jpg)