Bitcoin

Bitcoin  Ethereum

Ethereum  Tether

Tether  XRP

XRP  BNB

BNB  USDC

USDC  Solana

Solana  TRON

TRON  Figure Heloc

Figure Heloc

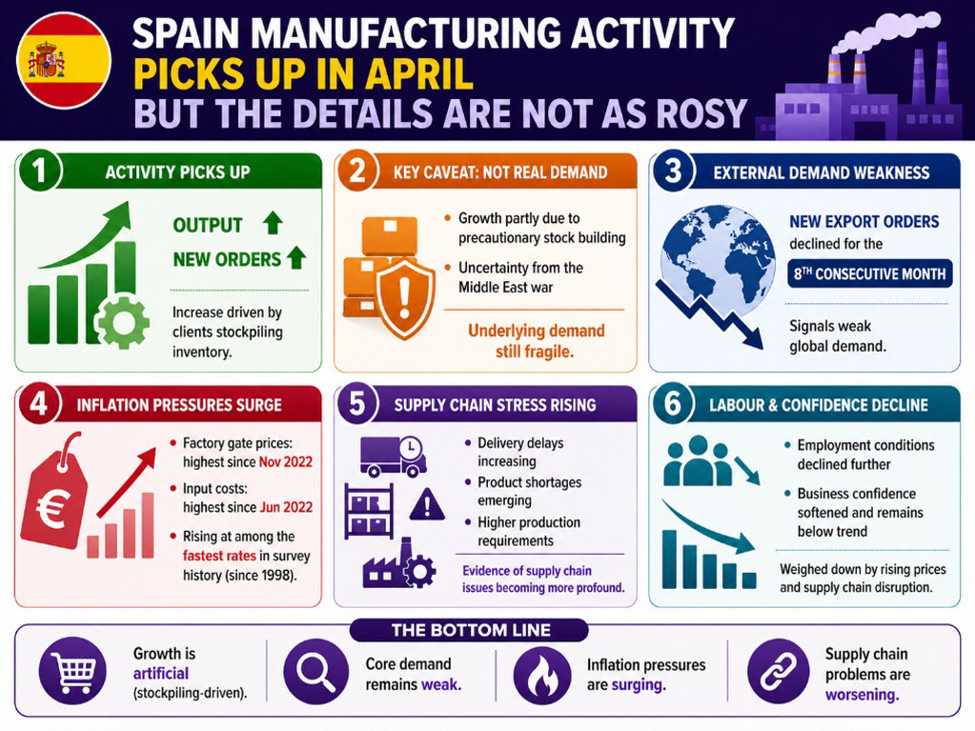

Manufacturing PMI 51.7 vs 49.5 expectedPrior 48.7That’s a surprising jump but the details show that it is mostly on the back of a notable push up in new orders and output as clients look to

secure stock. Of note, HCOB points out that “growth in new work however in part reflected client stock

building due to the uncertainty caused by the war in the

Middle East, especially in relation to supply chains, product

availability and prices”.Adding that underlying demand is still relatively fragile, as was the case with international demand, with new export orders declining

in April for an eighth successive month.Besides that, there was once again another considerable accelerations in inflation pressures. Factory gate prices rose at the steepest pace since

November 2022, which led to input prices increasing to the greatest degree since June 2022 and therefore at a

rate amongst the greatest seen in the survey history (which

began in early 1998).Meanwhile, delivery delays and higher production requirements were much more evident in April. That is evidence of supply chain issues starting to become more profound with product shortages also showing up.Rounding that off is a further drop in employment conditions and also softening confidence levels. The latter continues to run below trend amid over

price trends and supply chain disruption.HCOB notes that:“Spain’s manufacturing sector recorded growth of

both output and new orders in April, marking a positive

reversal from March’s outturn. However, lift the lid on

the latest data and growth was in part supported by

client inventory building as firms raced to secure goods

given the product shortages and supply disruption

caused by the war in the Middle East. Overall, sentiment

remains historically low, and firms are expressing

notable uncertainty in the outlook.

“Moreover, amid the energy shock and supply disruption,

input prices are rising at a severe rate and to a degree

not seen since mid-2022. Crucially the level of pass

through was also significant, with selling price inflation

picking up to its fastest level in just short of threeand-a-half years. Although there remains significant

uncertainty on the length and duration of the price and

supply shock, the willingness of a notable number of

firms to raise their prices increases the possibility of

second round inflation effects already being in play.”

This article was written by Justin Low at investinglive.com.

💡 DMK Insight

The unexpected rise in Manufacturing PMI to 51.7 signals potential economic resilience, but here’s the catch: it’s driven mainly by new orders, not broad-based growth. For traders, this could mean short-term bullish sentiment, especially in sectors tied to manufacturing and supply chains. However, the underlying details suggest caution; if new orders are merely stockpiling rather than sustained demand, we might see a pullback. Keep an eye on related assets like industrials and materials, as they could react strongly to this data. Watch for key resistance levels around 52.5 in PMI, which could indicate whether this uptick is a trend or a blip. Also, monitor the next few weeks for any shifts in consumer sentiment or further economic indicators that could confirm or contradict this PMI reading.

📮 Takeaway

Watch for PMI resistance at 52.5 and monitor new orders for signs of sustained demand; volatility could follow if expectations shift.