Bitcoin

Bitcoin  Ethereum

Ethereum  Tether

Tether  XRP

XRP  BNB

BNB  USDC

USDC  Solana

Solana  TRON

TRON  Figure Heloc

Figure Heloc

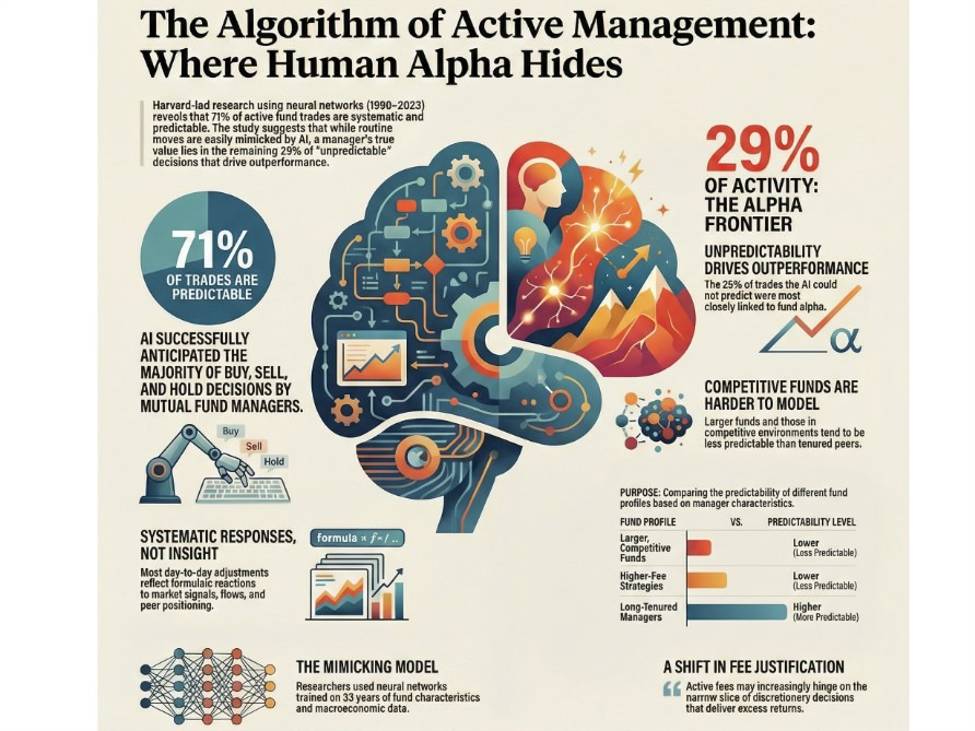

Harvard-led research suggests AI can replicate most active-fund trading patterns, leaving true alpha concentrated in a smaller set of non-routine decisions.Summary:AI model predicted 71% of fund tradesNeural network trained on 1990–2023 dataUnpredictable trades linked to outperformanceRoutine activity appears systematicLarger, competitive funds less predictableActive-fee justification under scrutiny(ps. I bolded the really interesting part below)A new academic study led by researchers at Harvard Business School suggests that much of active fund management follows patterns sophisticated algorithms can learn, raising fresh questions about the value of stock-picking fees.The working paper, titled Mimicking Finance and published via the National Bureau of Economic Research, uses a neural-network model trained on rolling five-year windows between 1990 and 2023. Drawing on fund characteristics, investor flows, stock attributes and macroeconomic data, the system was able to predict roughly 71% of mutual fund trading decisions, whether a manager would buy, sell or hold a stock over a given quarter.The findings suggest that a large share of day-to-day portfolio adjustments reflects systematic responses to flows, market signals and peer positioning rather than purely idiosyncratic insight. In effect, machines appear capable of replicating much of the industry’s common playbook.However, the study’s most revealing insight lies in what the model could not anticipate. The remaining 29% of trades, those that departed from detectable patterns, were more closely associated with outperformance. That implies that genuine alpha may reside in the smaller set of non-routine decisions that deviate from formulaic behaviour.The authors argue that machine-learning tools are better suited than traditional linear factor models to capture the complex ways managers react to shifting conditions. Yet the model predicts trade direction, not size, and further refinements are planned.Predictability also varies across managers. Larger funds, higher-fee strategies and teams operating in more competitive environments tended to be less predictable, while longer-tenured managers or those overseeing multiple products were more so.For the active management industry, already under pressure from low-cost passive products tracking benchmarks such as the S&P 500, the implications are economic rather than existential. If most routine trades can be anticipated algorithmically, fee justification may increasingly hinge on the narrower slice of genuinely discretionary decisions that deliver excess returns.The study underscores a broader distinction: while predicting market moves remains notoriously difficult, predicting professional behaviour may be far easier.Source: Bloomberg (gated)

This article was written by Eamonn Sheridan at investinglive.com.

💡 DMK Insight

AI’s ability to predict 71% of fund trades is a game changer for active management. This research highlights a crucial shift in how traders might view active funds. If AI can replicate routine trading patterns, the justification for high active fees comes into question. Traders should be wary of funds that rely heavily on predictable strategies, as they may struggle to deliver true alpha. The implication here is that smaller, more agile funds that can make non-routine decisions might outperform larger competitors. This could lead to a reallocation of capital towards these nimble funds, impacting their performance metrics and fee structures. Watch for how fund managers respond to this research. If they start emphasizing unique, unpredictable strategies, it could signal a broader trend in the market. Keep an eye on fund flows and performance metrics over the next quarter to gauge shifts in investor sentiment towards active versus passive management.

📮 Takeaway

Monitor fund flows and performance metrics closely; a shift towards smaller, agile funds could reshape active management strategies in the coming months.