Bitcoin

Bitcoin  Ethereum

Ethereum  Tether

Tether  BNB

BNB  XRP

XRP  USDC

USDC  Solana

Solana  Figure Heloc

Figure Heloc

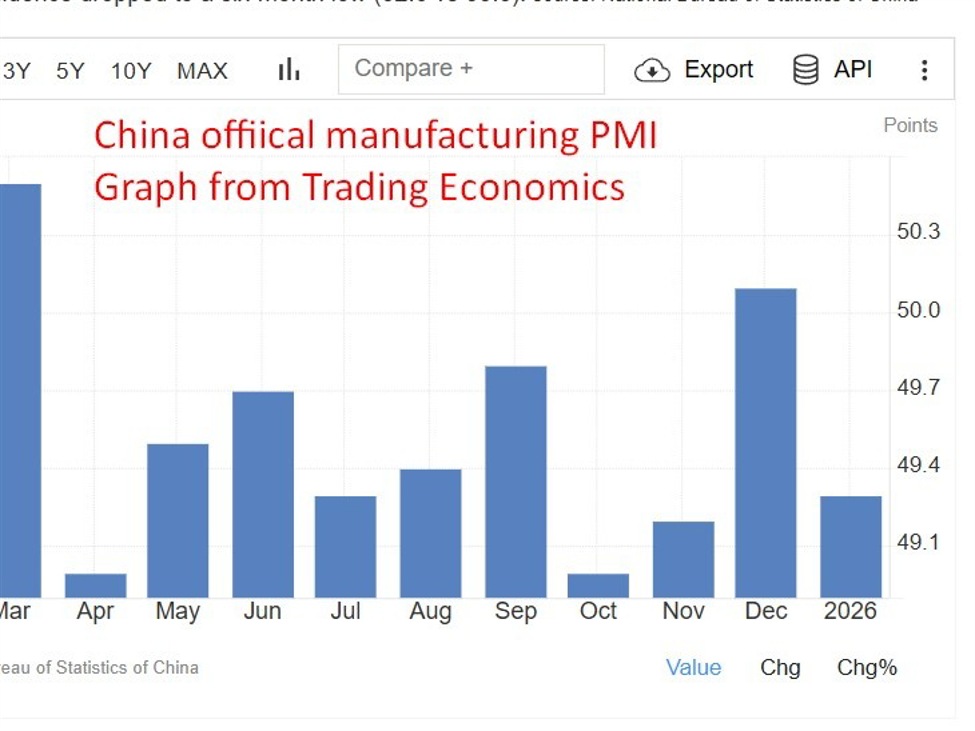

Summary:China’s official PMI data point to persistent domestic weakness at the start of 2026, according to analysis from ING.The official manufacturing PMI fell back into contraction, reinforcing doubts that December marked a genuine turning point.Price indicators showed tentative improvement, offering some relief from deflation concerns.Private-sector PMI data painted a more constructive picture, highlighting the role of exports and private firms.Services activity also slipped into contraction, underscoring the challenge of reviving domestic demand.China’s softer-than-expected PMI readings in January suggest that domestic economic challenges have carried over into the start of 2026, even as external demand continues to provide pockets of support, according to analysis from ING Group.The official manufacturing purchasing managers’ index slipped back into contractionary territory at 49.3 in January, down from 50.1 in December and well below market expectations for a second month of expansion. The setback reinforces concerns that December’s improvement may have been temporary rather than the start of a sustained recovery. Manufacturing activity has now been in contraction for nine of the past ten months, highlighting the fragility of underlying demand conditions.ING noted that the weakness was broad-based across most sub-indices. Production remained marginally in expansion but slowed notably, while new orders fell back below the 50 threshold, erasing December’s gains. Export orders also deteriorated, pointing to softer momentum even as overseas demand remains comparatively stronger than domestic consumption. Other indicators, including employment and order backlogs, edged lower, reinforcing the picture of subdued factory activity.There were, however, some tentative positives in the price data. Measures of ex-factory prices moved into expansion for the first time in almost two years, while raw material input costs rose to their highest levels in around 20 months. ING views these developments as encouraging signs in the context of China’s long-running deflation concerns, even if they do not yet signal a broader turnaround in demand.The official PMI also highlighted a growing divergence by firm size. Large enterprises continued to outperform, remaining in expansionary territory, while small and medium-sized firms stayed under pressure—an outcome consistent with tighter financing conditions and weaker domestic demand.In contrast, private-sector survey data painted a more optimistic picture. The RatingDog manufacturing PMI edged higher in January, supported by gains in production, new orders and employment, alongside rising output prices. ING noted that this divergence reflects differences in survey coverage, with the private PMI skewed more toward export-oriented and privately owned firms, which have benefited from stronger external demand.The contrast echoes a key theme from 2025, when exports and industrial output held up relatively well while household demand and services lagged. That imbalance was also evident in the non-manufacturing PMI, which slipped back into contraction in January, hitting its weakest level in more than three years. Services indicators such as new orders softened again, underscoring the difficulty policymakers face in shifting growth toward domestic consumption.Overall, ING concludes that China’s PMI data point to stabilisation rather than recovery. Without a more durable pickup in domestic demand, the economy is likely to remain reliant on external drivers and policy support as 2026 unfolds.

This article was written by Eamonn Sheridan at investinglive.com.

💡 DMK Insight

China’s PMI data just dropped back into contraction, and here’s why that matters: For traders, this signals ongoing domestic weakness that could impact global markets. A declining manufacturing PMI suggests that demand is faltering, which could lead to further economic stimulus measures from the Chinese government. This is crucial for forex traders, especially those focused on the yuan, as any additional easing could weaken the currency further. Keep an eye on related markets like commodities, as lower demand from China often translates to reduced prices for industrial metals and energy. On the flip side, the slight uptick in price indicators might hint at a potential stabilization, but it’s too early to call a trend. Traders should watch the 50 level on the PMI closely; a sustained move below this could trigger bearish sentiment across Asian markets. If you’re in forex, consider monitoring the USD/CNY pair for volatility as these data points unfold. The next few weeks will be critical for gauging whether this is a temporary dip or a sign of deeper economic issues.

📮 Takeaway

Watch the 50 level on China’s PMI; a sustained drop could signal further yuan weakness and impact global markets.